By Fredrik Lindstrom · ~12 minute read · May 2026

In conference rooms from London to Singapore, the same scene plays out. A consultant pulls up a slide titled “Customer Experience Roadmap.” Boxes flow left to right: marketing, sales, service. Arrows imply integration. The CFO asks the predictable question — what’s the ROI? — and the room nods through a slide deck that doesn’t actually answer it.

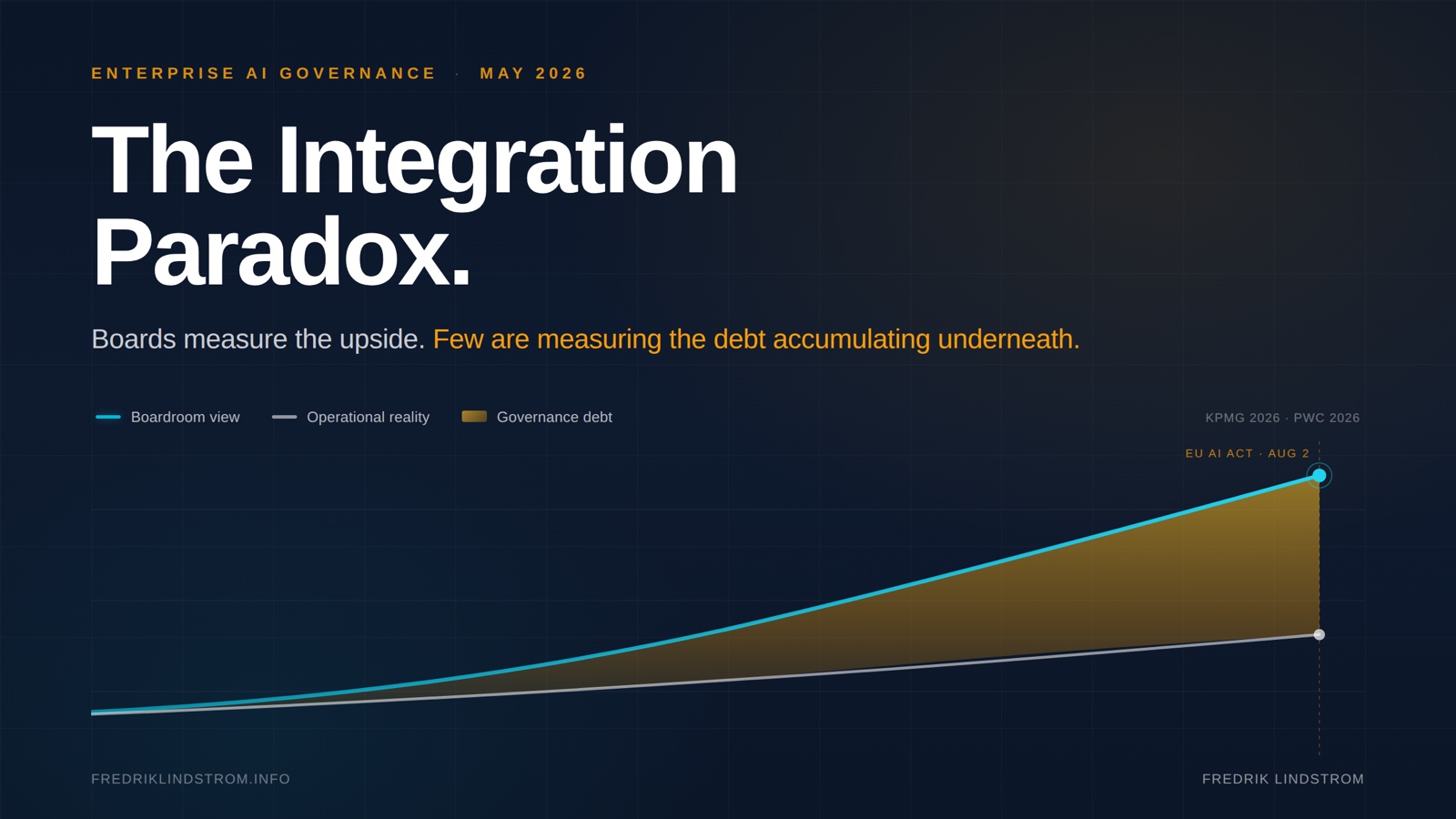

Two weeks ago, KPMG published a study of 300 customer-facing executives that should have stopped every CRO, CMO, and CIO in their tracks. Eighty-seven percent agree that integration of marketing, sales, and service is the path to growth. Five percent have actually achieved it. Read that again. Nineteen out of every twenty companies agree on the strategy and can’t execute it.

Eighty-seven percent agree on the strategy. Five percent execute it. That isn’t a strategy problem. It’s a definition problem.

This isn’t a fringe finding. PwC’s 2026 AI Performance Study, published the same month and based on 1,217 senior executives across 25 sectors, surfaces the same gap from the value side: 20% of companies capture 74% of AI-driven returns. The AI-fit cohort delivers 7.2 times the financial performance of everyone else. Same companies, different research methodology, identical conclusion: integration capability is the ROI gate.

I’ve spent 25 years in cybersecurity and enterprise technology watching transformations stall in exactly this pattern. Leaders mistake structural alignment for true integration. They redraw org charts. They form steering committees. They consolidate vendors. They migrate to a unified CRM. And then they wonder why the customer experience still feels disconnected — why the marketing pitch doesn’t match the sales conversation, why service has no idea what was promised at the point of sale.

The gap isn’t a strategy problem. It isn’t a budget problem. It’s a definition problem. And the next 14 weeks — between now and the August 2 enforcement deadline of the EU AI Act’s high-risk system requirements — will separate the companies that understood the difference from the ones that didn’t.

This article walks through the five forces compressing the integration timeline: the impasse KPMG and PwC measure from different sides, the regulatory cliff in Europe, the speed advantage in Asia-Pacific, the security blind spot nobody is writing about, and the change management lie that keeps making transformations fail. By the end, you’ll have a clearer picture of where your organization actually sits on the integration curve — and what to do about it before regulators, competitors, or your own customers force the question.

The impasse — what KPMG and PwC measure from different sides

KPMG’s framing is structural. Their report calls the 87/5 gap an “impasse” and traces it to a category error: leaders treating org-chart redesign as if it were the same as a unified data and intelligence layer. One creates the appearance of integration. The other creates the capability.

PwC’s framing is financial. Their study found that companies with strong AI foundations get double the ROI from each new use case compared to those without. “Doing more AI” without the integration layer underneath produces what their researchers call a low conversion rate — activity without outcomes.

Activity without outcomes. Pilots without scale. Tech investment without business reinvention. The pattern repeats across every region we surveyed.

Both consultancies arrive at the same diagnosis through different doors. Integration isn’t a technology problem you solve once. It’s a capability you compound — or fail to. The 5% of companies KPMG flags as fully integrated overlap heavily with the 20% PwC flags as AI leaders, and the math compounds: AI-fit companies are 2.6 times as likely to say AI has helped them reinvent their business model, and 1.5 times as likely to provide dedicated infrastructure for AI experimentation. Integration capability turns into AI ROI which turns into market position which funds the next round of integration. The companies on the wrong side of this curve aren’t standing still. They’re falling behind faster every quarter.

KPMG also identifies four recurring blockers: technology, data, organizational silos, and change. The pattern in their data is striking — most companies see integration as a project with an end state. Build the unified CRM. Migrate the data. Realign the teams. Done. But the highest-performing 5% treat it as a maturity curve: enable, embed, evolve, value, maturity. The difference is whether you stop after the technology lift or keep going through the cultural and operational redesign that makes the technology actually work.

Most don’t.

Europe’s regulatory reality check — when integration becomes a legal obligation

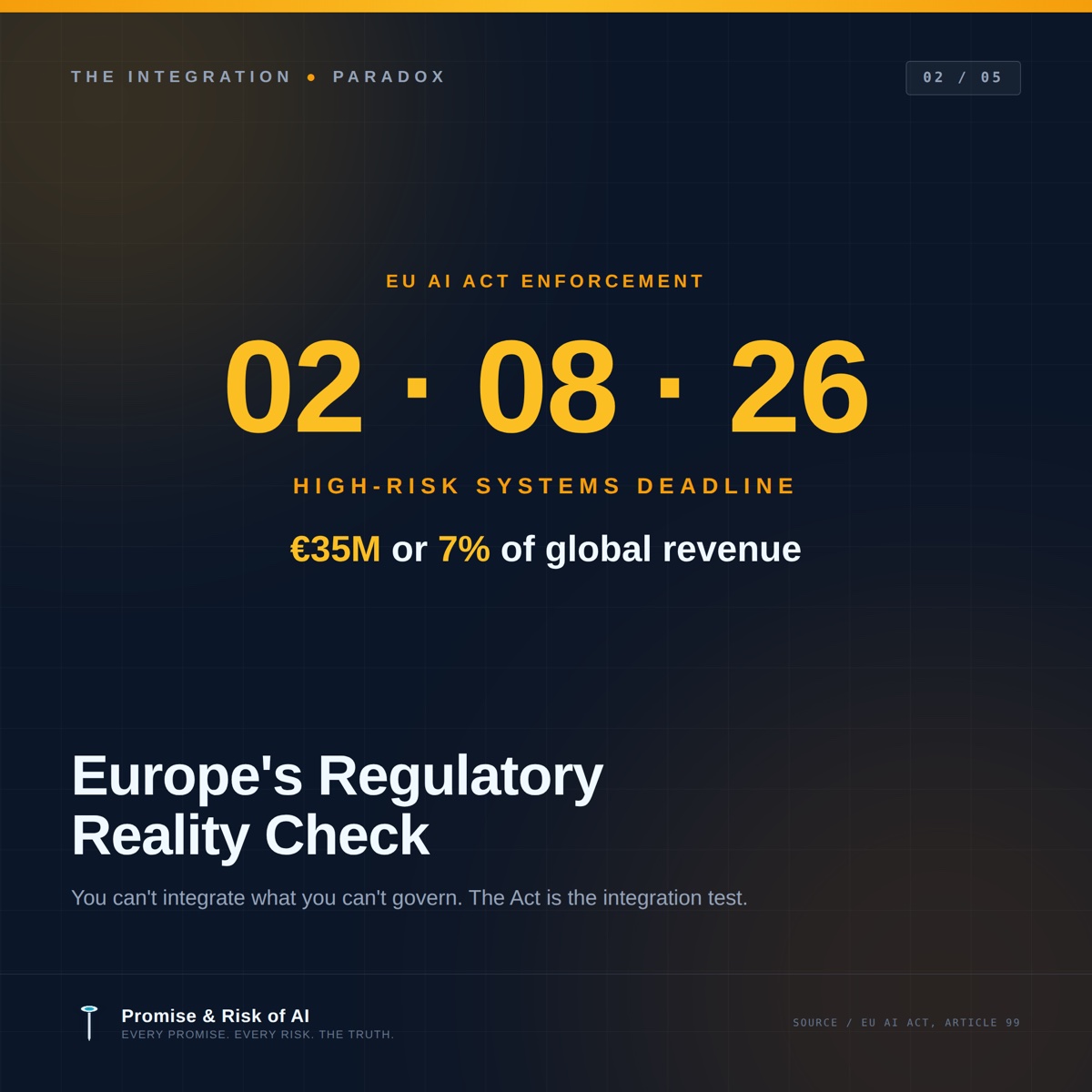

Fourteen weeks.

That’s how long European enterprises have until the EU AI Act’s high-risk system requirements become enforceable on August 2, 2026. Reading the KPMG report from a European boardroom should produce a different reaction than reading it from a US one — because in Europe, the integration question stops being optional well before the next budget cycle.

Here’s what the regulatory regime looks like in practice:

- Penalties: up to €35 million or 7% of global revenue for prohibited AI uses; €15 million or 3% for high-risk system non-compliance

- Compliance cost per high-risk system: €180,000 to €420,000, according to the European Commission’s own impact assessment

- Deployment delay: 4 to 7 months added to AI project timelines, per European Policy Centre analysis

- Specialist deficit: more than 400,000 AI and data science professionals short across the EU by 2026 (Cedefop)

And yet, against that headwind, Europe’s enterprise AI market is projected to grow at a 33.76% CAGR from 2026 to 2034, reaching $197 billion. The regulation isn’t slowing the market. It’s separating the prepared from the unprepared.

The Act isn’t a compliance hurdle. It’s the integration test. You cannot legally integrate customer data for AI use cases without governance baked in from the start.

The KPMG report identifies four blockers to integration. In Europe, there’s a fifth that doesn’t appear anywhere in their report: governance. And in Europe, governance isn’t a parallel workstream — it’s the integration foundation. You cannot legally combine customer data across marketing, sales, and service for AI use cases without three artifacts in place:

- DPIA — Data Protection Impact Assessment under GDPR Article 35

- FRIA — Fundamental Rights Impact Assessment under EU AI Act for high-risk systems

- Risk management framework — mapped to NIST AI RMF or ISO/IEC 42001

These are not “compliance” in the box-checking sense that audit functions tend to default to. They are the structural prerequisites for integrated AI in any customer-facing workflow that touches an EU resident. The companies that built privacy-by-design from the GDPR era have a head start. Everyone else is reverse-engineering governance into systems already in production — which the European Commission’s own guidance flags as the most expensive path.

There’s a second-order effect worth flagging. The Act applies extraterritorially. A US-headquartered enterprise serving EU customers from a unified CRM in a US-region cloud is in scope. The integration problem isn’t “do we have one customer view” — it’s “can we prove the AI components touching that customer view are auditable, explainable, and accountable to a regulator who has not yet asked.”

The boards that treat August 2 as the integration deadline will be the ones still operating in 2027 with their reputations intact. The boards treating it as a separate compliance track — bolted onto the side of an integration program that’s already shipped — will be the ones explaining to regulators why their unified customer platform is also an unaccountable AI system.

APAC’s speed advantage — what happens when capital and policy align

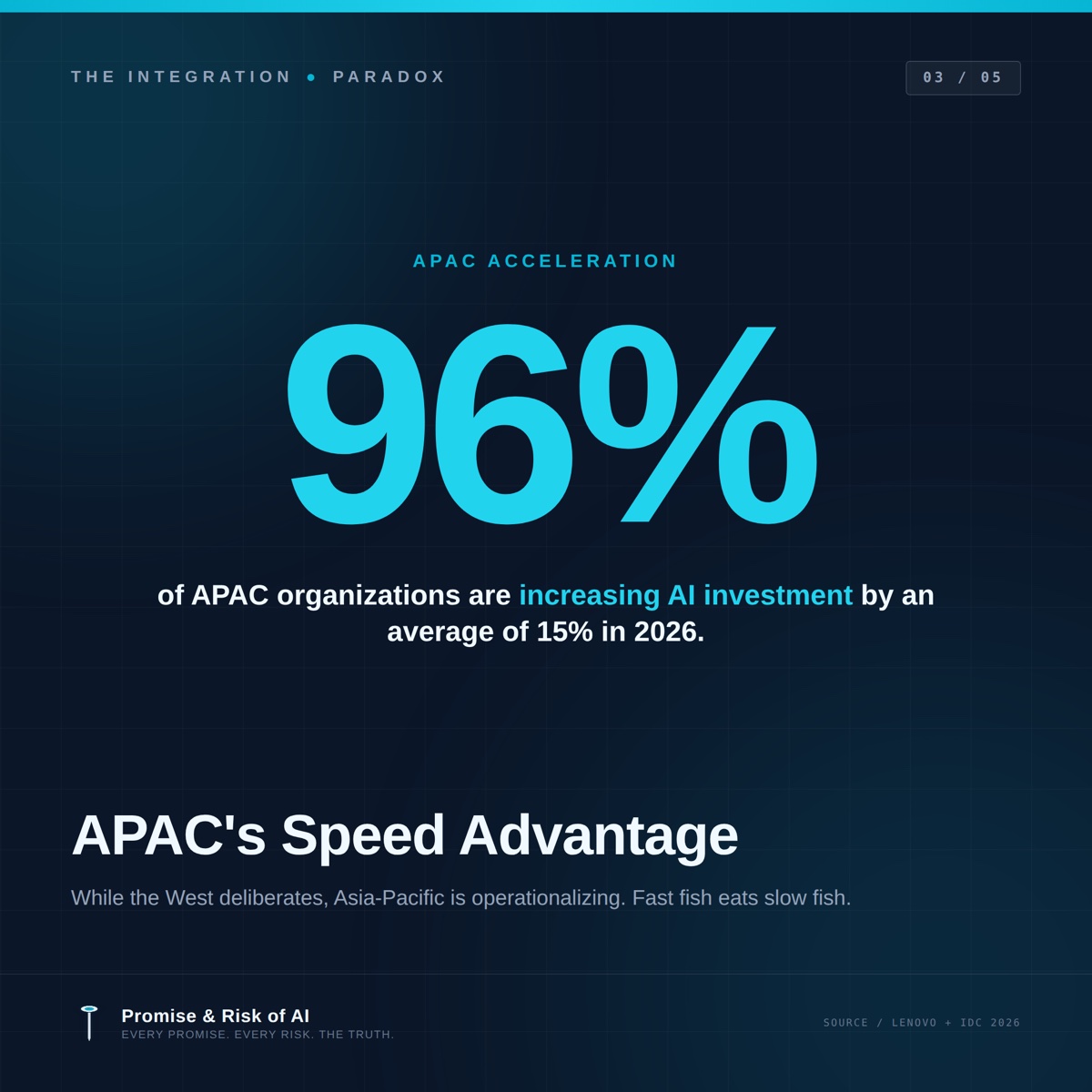

Two stats from Asia-Pacific should make every Western boardroom uncomfortable:

- 96% of APAC organizations are increasing AI investments by an average of 15% in 2026 (Lenovo / IDC, n=920)

- 70% expect agentic AI to disrupt their business model within 18 months (IDC FutureScape APeJ)

Compare those numbers to the KPMG finding: 87% of US customer-facing leaders believe integration is the path. Only 5% have achieved it. Different region. Different mindset. Different outcome.

What APAC is doing differently

Capital is moving on a different timeline. 88% of APAC organizations expect ROI from AI projects this year — anticipating $2.85 returned for every $1 invested. Not in three years. This year.

The CIO isn’t writing the only checks. Half of all AI initiatives in APAC are now funded by non-IT departments. Marketing, finance, and business unit budgets are doing what was traditionally IT’s job. That sounds like a governance risk — and in some cases it is — but it also unlocks faster experimentation cycles than centralized funding allows.

Singapore is the bellwether. 54% of large Singaporean organizations have already deployed AI PCs, 12 percentage points above the regional average. Government policy and enterprise capital are aligned in a way the West hasn’t seen since the early days of cloud adoption — when AWS shipped before any meaningful regulation existed.

AI factories are getting built. IDC predicts that by 2028, 65% of A2000 enterprises in APAC will operate AI factories as core infrastructure: centralized environments combining infrastructure, models, data, and governance into repeatable pipelines. That’s not a 2026 story — it’s a 2026 commitment to a 2028 capability.

Speed without integration isn’t velocity. It’s expensive movement. The fast fish in this metaphor is the one that solved its data problem first.

But the headline narrative misses the part that matters most. APAC’s speed advantage isn’t speed for its own sake. It’s speed grounded in data foundations. The same SAP research that found only 46% of brands globally can connect data well enough to power AI sustainably also confirmed that APAC organizations are leading on the unified data layer that makes integration possible. Singapore, Australia, and South Korea aren’t just deploying AI faster — they’re deploying it on top of better-organized customer data.

“Fast fish eats slow fish” is the framing you’ll hear at every APAC technology conference this year. But the fast fish in this metaphor isn’t moving fast for its own sake. It’s the one that solved its data problem first. Speed without integration isn’t velocity — it’s expensive movement.

The strategic question for Western enterprises isn’t “are we moving fast enough.” It’s a different question Deloitte’s 2026 State of AI report surfaces: are we optimizing existing processes around AI, or are we transforming the architecture? Only 34% of organizations are doing the latter. The 5% that KPMG flags as fully integrated overlap heavily with the 34% Deloitte flags as transformers — and both overlap with the 20% PwC flags as AI leaders. The cohort is small, and it’s pulling away.

The security blind spot — what KPMG didn’t write

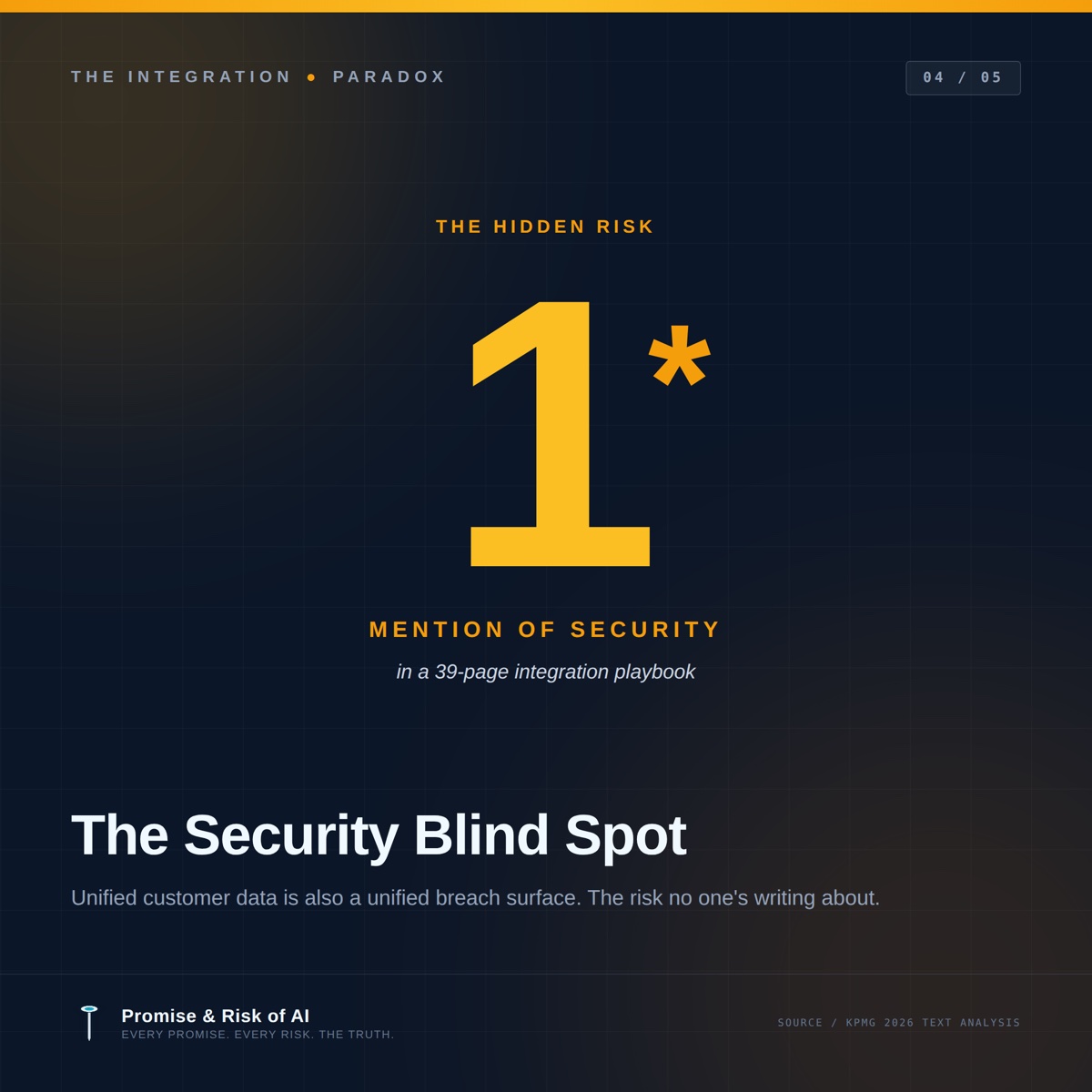

I read all 39 pages of the KPMG 2026 Customer Advisory report on integration. Security is mentioned exactly once.

In a 39-page playbook on unifying customer data across marketing, sales, service, finance, and HR — built on a vision of “shared intelligence” and AI agents acting in concert — security shows up as a 36% blocker to AI implementation. Then it disappears.

This is the integration story nobody is writing. After 25 years in cybersecurity, here’s the pattern I see repeating: every “unified” system is also a unified attack surface. The same architecture that enables real-time personalization across the customer journey also enables real-time data exfiltration if a single integration point is compromised. The boards asking “what’s our integration ROI” without asking “what’s our integration breach radius” are setting up the next generation of incident headlines.

Unified customer data is also a unified breach surface. The risk grows exactly as fast as the integration succeeds.

Three risks that rarely make the analyst slide deck:

1. Concentration risk in unified CRMs

The unified CRM platform that 61% of organizations are using as their integration approach (KPMG) becomes the highest-value target in the enterprise. One identity provider compromise. One misconfigured API. One vendor breach. Your entire customer relationship — marketing history, sales conversations, service tickets, billing data, behavioral analytics — is exposed at once, not in fragments. Pre-integration, an attacker had to chain three systems to get a complete customer picture. Post-integration, one breach gives them everything.

This is the inverse of the integration value proposition. Integration creates value by collapsing data silos. It creates risk by collapsing those same silos.

2. Shadow AI agents

Twenty-eight percent of APAC organizations have already deployed AI agents. Another 32% plan to within 18 months. Lenovo’s research with IDC explicitly warns that traditional identity and access management models break when agents delegate to other agents — creating identity sprawl with no audit trail. KPMG’s “shared intelligence” vision becomes shadow AI at enterprise scale if every agent isn’t a registered, auditable entity with an owner, a purpose, and an off-switch.

Most enterprises don’t have an agent registry. Most don’t have a process to approve a new agent into production. Most can’t tell you, today, how many AI agents are running against their customer data. That’s not a hypothetical risk. That’s the current state.

3. Hallucinations in customer-facing workflows

Seventy-eight percent of organizations expect agentic AI to handle at least half of customer support within 18 months (Adobe 2026). When an agent invents a refund policy, a product specification, or a contract term and a customer relies on it, the legal and reputational exposure isn’t theoretical. The Mata v. Avianca case taught the legal profession this lesson in 2023, when an attorney filed a federal brief built on AI-fabricated case law. Customer-facing AI is heading for the same lesson at enterprise scale, and the case law won’t be sympathetic the second time around.

When did your CRM last get a threat model? If the answer is “never,” your integration program is shipping a vulnerability surface, not a customer experience.

The fix isn’t bolted-on security. It’s security-by-design integration:

- NIST AI Risk Management Framework as the governance baseline — the publicly available framework that every regulator references and most enterprises haven’t operationalized

- ISO/IEC 42001 for AI management systems — the certifiable standard that turns governance from policy into auditable practice

- An agent registry with full lifecycle management — every agent has an owner, a purpose, a sunset date, and an off-switch

- Threat models for the unified data layer — treated as a critical asset class, not a CRM module

None of this is exotic. All of it is in the published guidance from NIST, ISO, and ENISA. What’s missing is the bridge from the integration program plan to the security architecture — and that bridge is exactly where the 5% of fully integrated companies separate from the 95%.

The change management lie — why technology gets the budget and people get the blame

The most damning chart in KPMG’s report isn’t about technology. It’s about people.

Only 19% of organizations invest in cross-functional training as part of their integration approach. Yet when integration fails, 50% of leaders blame employee confusion or resistance. We invest in technology. Then we blame humans for not adopting it.

The technology gets the budget. The people get the blame. Then we hire a new vendor, run the same play, and act surprised when it fails again.

This is the change management lie — and it’s the one consistent reason CRM projects, integration initiatives, and AI deployments fail in cycle after cycle.

The numbers should reframe every transformation budget conversation:

- 30% of CRM implementations are still considered failures (Searchlab 2026)

- 43% of those failures are attributed to poor user adoption

- 28% are attributed to bad data quality

- Companies investing meaningfully in change management are 3.5x more likely to succeed

- Employees at AI-leading organizations are 2.1x more likely to trust AI-generated insights and act on them in day-to-day work (PwC 2026)

The pattern: technology gets the budget, people get the blame, data gets ignored, and the cycle repeats with a new vendor logo. KPMG’s data confirms it from another angle — 62% of organizations facing negative integration outcomes report cultural resistance and misaligned goals. The technology was fine. The humans were never brought along.

Three principles that change the equation

First, treat 15–20% of integration budget as a floor for adoption — not a stretch goal.

KPMG explicitly recommends 15–20% of integration budget for change enablement. Most enterprises spend less than 5%. The math is brutal: a 30% project failure rate is cheaper to prevent at 15% adoption spend than to repeat at 100% reimplementation cost. PwC’s data quantifies what that investment actually buys — a 2.1x lift in employee trust and adoption. Trust isn’t a soft outcome. It’s a throughput constraint. Low trust means low use means low impact.

Second, build hybrid roles, not just cross-functional teams.

Only 24% of organizations create roles spanning marketing, sales, and service. Cross-functional teams without cross-functional roles are committee-by-another-name. The unified data layer demands a unified job description — someone whose career path runs across the integration, not perpendicular to it. The CDO and the CMO need a shared deputy, not a steering committee.

Third, make AI fluency a workforce capability, not a leadership rhetoric.

Anthropic’s 4D Framework — Delegation, Description, Discernment, Diligence — is the clearest model I’ve seen for individual AI fluency at enterprise scale. Free, certificate included, takes less than a day. If your integration roadmap depends on AI agents and your workforce can’t articulate when to delegate, how to describe a task, where discernment is required, and what diligence looks like, you don’t have an integration roadmap. You have a press release.

The companies winning at integration aren’t the ones with the best CRM. They’re the ones who treat their workforce as integration infrastructure — and budget accordingly.

Where this leaves you, between now and August 2

Fourteen weeks isn’t a long runway, but it’s enough to take an honest measurement.

Walk into your next executive review and ask five questions. Where on the maturity curve does our integration program actually sit — enable, embed, evolve, value, or maturity? Have we conducted a FRIA and DPIA on every customer-facing AI system that touches an EU resident? What’s our agent registry, and who owns it? What percentage of our integration budget is allocated to change management — and is the answer above or below 15%? And the question that ties them all together: when our customer data layer becomes our highest-value target, who in the organization owns the threat model?

If your team can answer all five with specifics, you’re in the 5%. If they can answer three, you’re in the chasing pack — the 53% KPMG calls “highly integrated” but not yet fully there. If they can’t answer any, you’re in the 42% who are somewhere between somewhat-integrated and not-integrated, and the next four months will be expensive.

The advantage that the AI leaders already enjoy will only grow, because these companies are learning fast, redeploying solutions faster, and safely automating decisions. PwC frames it as a compounding performance premium. KPMG frames it as the impasse most companies fail to break through. Both are right.

Integration isn’t a project. It’s a capability. And the next 14 weeks will tell you which side of that line your organization sits on.

Fredrik Lindstrom is the founder of Promise & Risk of AI, a YouTube channel and LinkedIn publication delivering balanced, honest AI literacy to business leaders. With 25+ years in cybersecurity and enterprise technology, his work focuses on the intersection of AI capability and organizational governance.

Every promise. Every risk. The truth.

Sources & methodology notes

All statistics in this article are drawn from publicly available 2025–2026 research. Where research methodologies differ, the differences are flagged in-text. Self-reported data is noted as such.

Primary sources

- KPMG 2026 Customer Advisory Research — Total Experience: Integrate to differentiate — and win. 300 customer-facing executives in US-headquartered organizations, fielded August–September 2025. Methodology note: 100% US-headquartered sample; impact data is self-reported.

- PwC 2026 AI Performance Study — Want ROI from AI? Go for growth. 1,217 senior executives across 25 sectors, fielded October–November 2025. 91% of respondents from publicly listed companies; 76% with $1B+ revenue.

- Lenovo / IDC CIO Playbook 2026 — 920 APAC technology leaders.

- IDC FutureScape 2026 — Worldwide AI and Automation Predictions for Asia/Pacific (excluding Japan).

- Adobe 2026 AI and Digital Trends Report — 3,000 executives + 4,000 customers globally.

- SAP 2026 Global Customer Engagement Index.

- Deloitte 2026 State of AI in the Enterprise — 3,235 leaders globally.

- Searchlab CRM Statistics 2026 (failure rate analysis).

- Dell Technologies / IDC InfoBrief — Future-Ready Workforce: AI PC Adoption (720 APAC ITDMs).

Regulatory & framework references

- EU AI Act — Articles 6, 11–15, 99. Penalty schedule and high-risk system obligations.

- European Commission AI Act impact assessment — compliance cost projections.

- European Policy Centre 2025 — deployment delay analysis.

- Cedefop (European Centre for the Development of Vocational Training) — AI specialist deficit forecast.

- NIST AI Risk Management Framework 1.0 (2023, revised 2025).

- ISO/IEC 42001:2023 — AI management systems.

- Anthropic AI Fluency: Framework & Foundations (4D Framework). Free course at anthropic.skilljar.com/ai-fluency-framework-foundations.

Cited cases

- Mata v. Avianca, Inc. (S.D.N.Y. 2023) — federal court sanctions for filing a brief built on AI-fabricated case law.