Where the US, EU, and Chinese AI vendors are heading over the next 18 months, and what each choice commits your enterprise to.

By Fredrik Lindstrom · ~13 minute read · July 2026

Walk into any enterprise AI strategy review in 2026 and three options sit on the table: an American frontier lab, a European sovereign challenger, and a Chinese open-weight house. The instinct is to line up their models and pick the best one. That instinct is the first mistake.

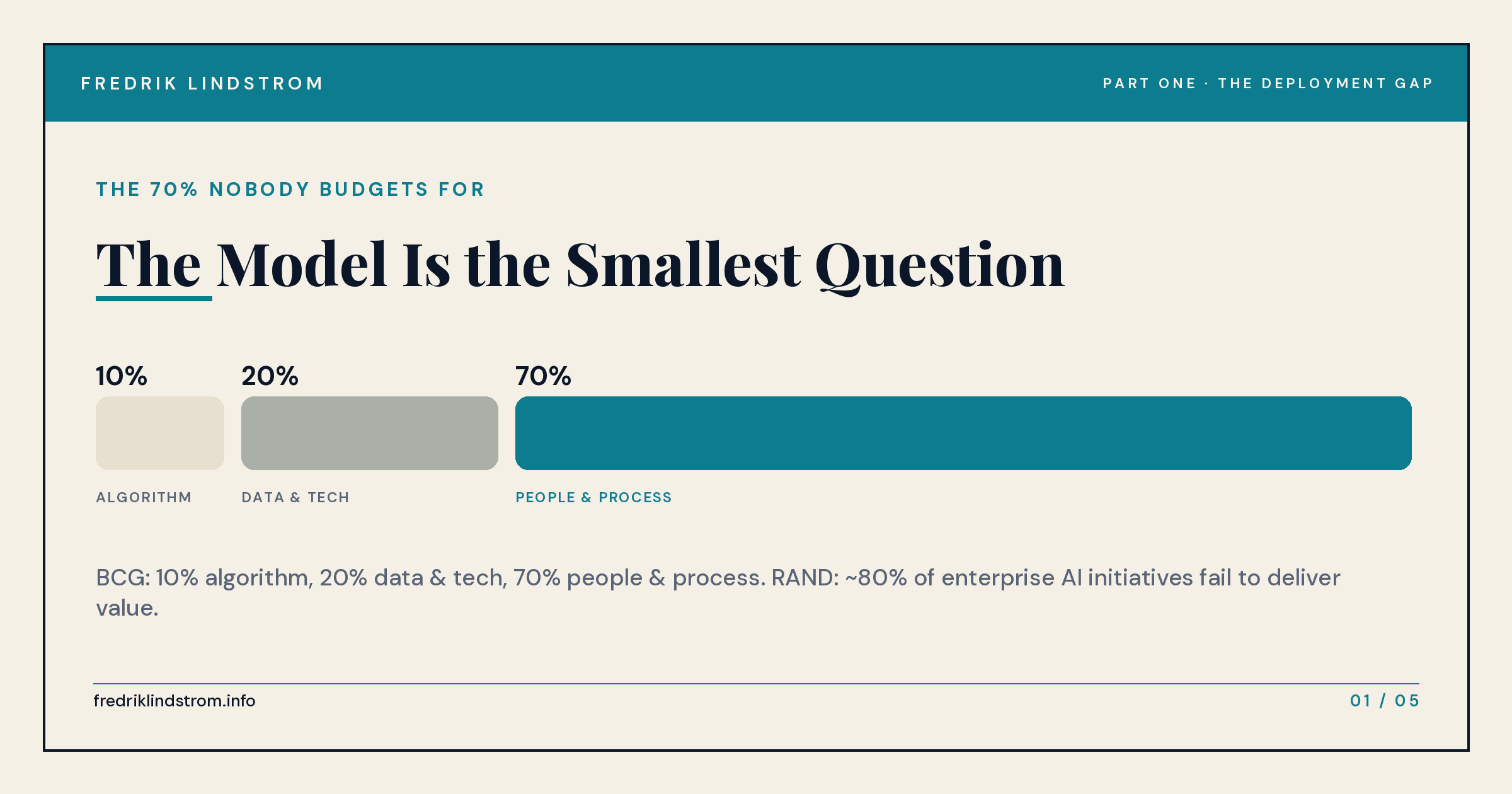

The model is roughly 10% of whether your AI program works. BCG has measured the ratio across years of deployments: 10% of the value comes from the algorithm, 20% from data and technology, and 70% from the people and process changes around it. RAND puts a harder number on the consequence. 80% of enterprise AI initiatives fail to deliver the value they promised — twice the failure rate of ordinary IT projects. MIT’s 2025 study of 300 deployments found that 95% of generative-AI pilots produced no measurable profit impact at all.

So the real question is not which model is best. It is which bet you are underwriting when you choose a vendor, and what that bet commits you to when it pays off, and when it doesn’t.

Each of the three blocs is making a different bet. The American labs are betting on capital and frontier capability, racing to public markets on the theory that scale wins. The Europeans are betting on regulation and sovereignty, that enterprises and governments will pay to keep AI under their own jurisdiction. The Chinese houses are betting on open weights and price, working to commoditize the exact layer the Americans are trying to own. All three bets are partly right. None of them is the thing your program will actually live or die on.

The 70% nobody budgets for

Start with the failure data, because it reorders everything that follows.

RAND’s breakdown is specific: of the 80% that fail, about a third are abandoned before production, a third reach production and deliver nothing, and the rest cannot justify their cost. Four of the five root causes RAND identifies are organizational, not technical. The model was rarely the problem. The translation layer between a working demo and a live operation was.

MIT’s finding is the one that should reshape procurement. Systems built with external partners succeeded roughly twice as often as internal builds, about two in three versus one in three. The build-it-yourself instinct, the one that feels cheaper and more sovereign, is statistically the one that fails. S&P Global watched the consequence land in a single year: the share of companies abandoning most of their AI initiatives rose from 17% to 42%, with an average of more than $7M written off per abandoned enterprise program.

I spent 25 years in cybersecurity services, and the shape of this is familiar. The organizations that bought the technology and ran at it alone stalled in the same place every time. The ones that succeeded brought in people who owned the deployment: the integration, the controls, the change management. They drove the outcome the technology had only promised. Same tools. Different result. The variable was never the product.

This is why the defining strategic move of early 2026 had nothing to do with a model. Within a few weeks, OpenAI stood up a deployment arm staffed with more than 150 forward-deployed engineers and over $4B, acquiring a specialist firm to do it. Anthropic launched a $1.5B services joint venture with Blackstone, Goldman Sachs, and Hellman & Friedman. Forward-deployed-engineering postings rose around 800% year over year. Every serious vendor is now racing to own the deployment layer, for one reason: a model is easy to swap, and a system that has been deployed into your workflows is not. That is where lock-in now lives, and where the next 18 months will be decided.

Hold that lens against each bloc.

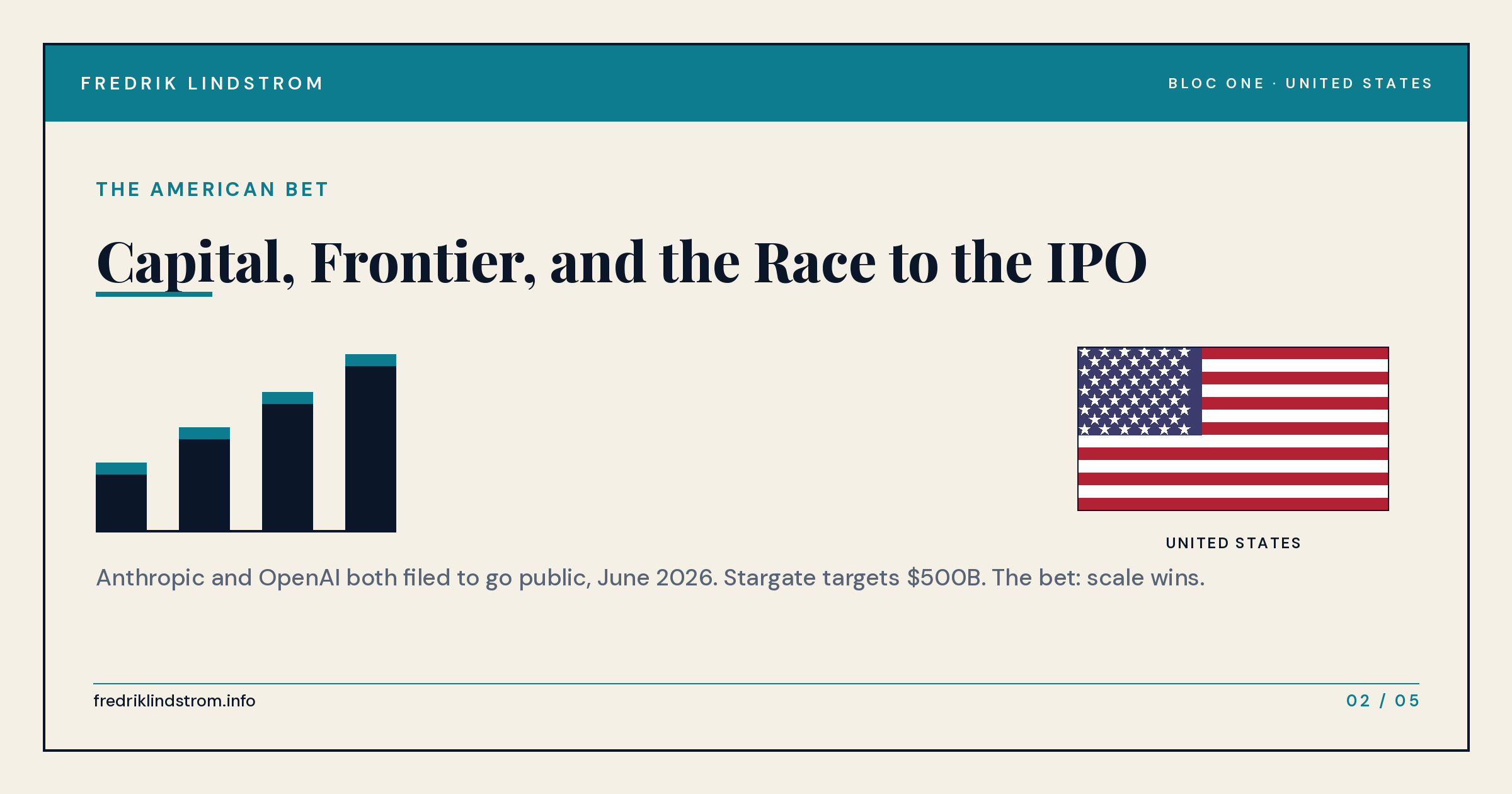

The United States: capital, frontier, and the race to the IPO

The American bet is the most straightforward and the best funded. Out-raise, out-compute, out-ship, and reach the scale where capital compounds faster than losses.

The numbers are real and they are large. Anthropic’s revenue ran from roughly $1B at the start of 2025 to a reported $30B run-rate by April 2026, driven heavily by enterprise and by Claude Code. OpenAI sits in the same range, growing about threefold a year, with around 800M weekly users. Both filed confidentially for public offerings in early June 2026. Google’s Gemini anchors the only true full-stack position, owning model, cloud, and its own TPU silicon, and Meta has abandoned open releases for a closed model and its three-billion-user distribution.

Two cautions belong in any board paper that cites these figures. First, the revenue numbers are contested: OpenAI publicly disputes Anthropic’s accounting, arguing the gross figure overstates the comparable number by around $8B, and the dispute will surface in IPO disclosures. Second, both companies are still deeply unprofitable, and the infrastructure buildout behind them runs on circular financing — NVIDIA, Oracle, and SoftBank investing in the same labs that buy their capacity. OpenAI’s Stargate program alone targets $500B and 10 gigawatts of power.

On capability, a procurement note that matters more than it looks. The models your contract will actually run in production are the deployed cohort — the generation that has cleared your security and compliance review, typically a year or more behind the frontier leaderboard. The gap between the best American lab model and the best European or Chinese model is real at the ceiling. It is much smaller, and sometimes irrelevant, for the workloads most enterprises actually run.

What you underwrite when you choose the American bloc: the deepest capability and ecosystem available, the strongest services bench now forming, and exposure to concentration risk, capital-market fragility, and US jurisdiction. The federal posture turned sharply deregulatory in late 2025, but a state-by-state patchwork persists. Texas, California, and Colorado all have AI laws live in 2026, so near-term compliance gets less certain, not more.

And US jurisdiction is not an abstraction. In June 2026, the Commerce Department ordered Anthropic to bar its newest model, Claude Fable 5, from every foreign national inside or outside the country, including Anthropic’s own foreign-born staff, over a claimed security bypass. Rather than comply selectively, Anthropic took the model offline worldwide, and as of mid-June the standoff with the White House was unresolved. A frontier model your European subsidiary is using one week can be gone the next, by government letter, with no say from you.

Europe: regulation as moat, sovereignty as product

The European bet is the one most aligned with where regulated enterprises and the public sector are heading. European buyers will pay to keep AI under European jurisdiction, and the rules will make that a competitive advantage rather than a cost.

Mistral is the flagship. It is reportedly raising around €3B at a roughly €20B valuation, which would roughly double its September 2025 round led by ASML. That figure is sourced to anonymous reporting and described as early-stage talks, so treat it as directional. Its real differentiator is not the model line. It is that the company is building owned compute on European soil: a data-center program targeting 200 megawatts by 2027, a training facility near Paris running on more than 13,000 NVIDIA chips, and a €1.2B build-out in Sweden on fully renewable power. Mensch’s own framing is that to deploy AI in the enterprise, you have to own the full stack.

Read that statement carefully, because it is the most important thing the European bloc has understood. Mistral has wrapped its model in a deployment platform — build, governance, custom model training on a customer’s own data — and a forward-deployed services motion, with named customers including BNP Paribas, TotalEnergies, Airbus, and several European governments. It is not selling a model. It is selling the 70% the failure data says actually decides the outcome, with a jurisdiction guarantee the American vendors structurally cannot match.

That guarantee is the whole point. Under GDPR, the AI Act, and the reach of the US CLOUD Act, a great many European public-sector and regulated workloads cannot legally sit on American-hosted infrastructure. Only EU-jurisdiction training and deployment resolves it.

The AI Act’s August 2026 milestone sharpens this, and it needs to be described accurately, because most coverage gets it wrong. It is the date most high-risk obligations and the enforcement regime were originally set to become applicable. It is not the moment the entire Act switches on. Prohibited uses applied in early 2025, the rules for general-purpose models applied in August 2025, and deployer transparency obligations still land on the August 2026 date.

What changed is the high-risk timeline itself. Brussels conceded in May 2026 that the original deadline was unworkable, with the technical standards and national authorities not ready in time, and reached a provisional agreement, the Digital Omnibus, to defer the core obligations for standalone high-risk systems by 16 months, to December 2027. That deferral is not yet law. It takes effect only on formal adoption and publication in the EU’s Official Journal, expected before August but not yet done, which means the prudent board plans to the original August 2026 date until the new one is actually published. Either way, the direction is fixed, and it favors vendors who built for it.

What you underwrite when you choose the European bloc: jurisdictional control, regulatory alignment, and a credible full-stack deployment story, bought at the cost of a genuine capability and scale gap and a far thinner capital base. Mistral has raised a few billion dollars against the American labs’ hundred-plus billion each. For sensitive and regulated workloads, that trade is often the right one. For frontier-dependent ones, it is a real constraint.

China: open weights, low price, and the commoditization play

The Chinese bet is the most disruptive to everyone else’s economics. Make the model layer cheap, open, and everywhere, so that no one can charge a premium for owning the frontier.

It is working on its own terms. Alibaba’s Qwen is the most-downloaded open-model family in the world, with more than 700 million downloads and over 100,000 derivative models built on it. In February 2026, Chinese models passed American ones in weekly token volume on one major routing platform for the first time. DeepSeek cut its pricing to roughly a quarter of the list rate and forced the whole market down with it. The best Chinese open models trail the top American proprietary models by single digits on composite benchmarks, and the gap is closing — though those benchmarks are largely vendor-published and thin on independent audit, which is its own reason for caution.

The constraint is silicon, and it is binding. Export controls cut off NVIDIA’s advanced chips, and the domestic alternative, Huawei’s Ascend line, sits well behind. By Huawei’s own roadmap, its 2026 chip is less capable than its best 2025 part, and the real bottleneck is high-bandwidth memory, where domestic supply covers only a fraction of demand. China can flood the world with good-enough inference. It cannot match American training compute at scale this cycle.

The deployment layer looks completely different here. There is no equivalent of the American services land grab, no forward-deployed-engineering arm. Chinese vendors operationalize through managed-service platforms, on-premise privatization, and national sovereign-AI partnerships across Southeast Asia and the Belt and Road. Two of them, MiniMax and Zhipu, went public in Hong Kong in January 2026 ahead of any American lab. MiniMax draws more than 70% of its revenue from outside China and carries no US listing restriction; Zhipu sits on the US Entity List.

What you underwrite when you choose the Chinese bloc: the lowest cost and genuinely open weights, against three hard constraints. Data routed to a Chinese-hosted API sits under PRC jurisdiction. Every model carries hard-coded content restrictions. And a US congressional committee opened investigations in 2026 into both the Chinese labs and the Western firms using their models. The mitigation that preserves the cost advantage is to run the open weights on your own or Western-managed infrastructure, which works technically, and which many enterprises still cannot do for compliance or brand reasons.

What a board should actually do

The three bets resolve into three different risk profiles, and the job is to match them to the work rather than to crown a winner.

For regulated, sovereign, and public-sector workloads, the European bloc and self-hosted open weights are the default; the August 2026 AI Act milestone turns jurisdictional alignment into an asset. For frontier capability and ecosystem depth, the American labs lead — but dual-source from the start, because the point of the deployment layer is precisely that it gets expensive to leave. For high-volume, cost-sensitive, non-sensitive work, Chinese open weights are viable, but only run on Western-managed or self-hosted infrastructure, never through a Chinese-hosted endpoint with anything sensitive in the payload.

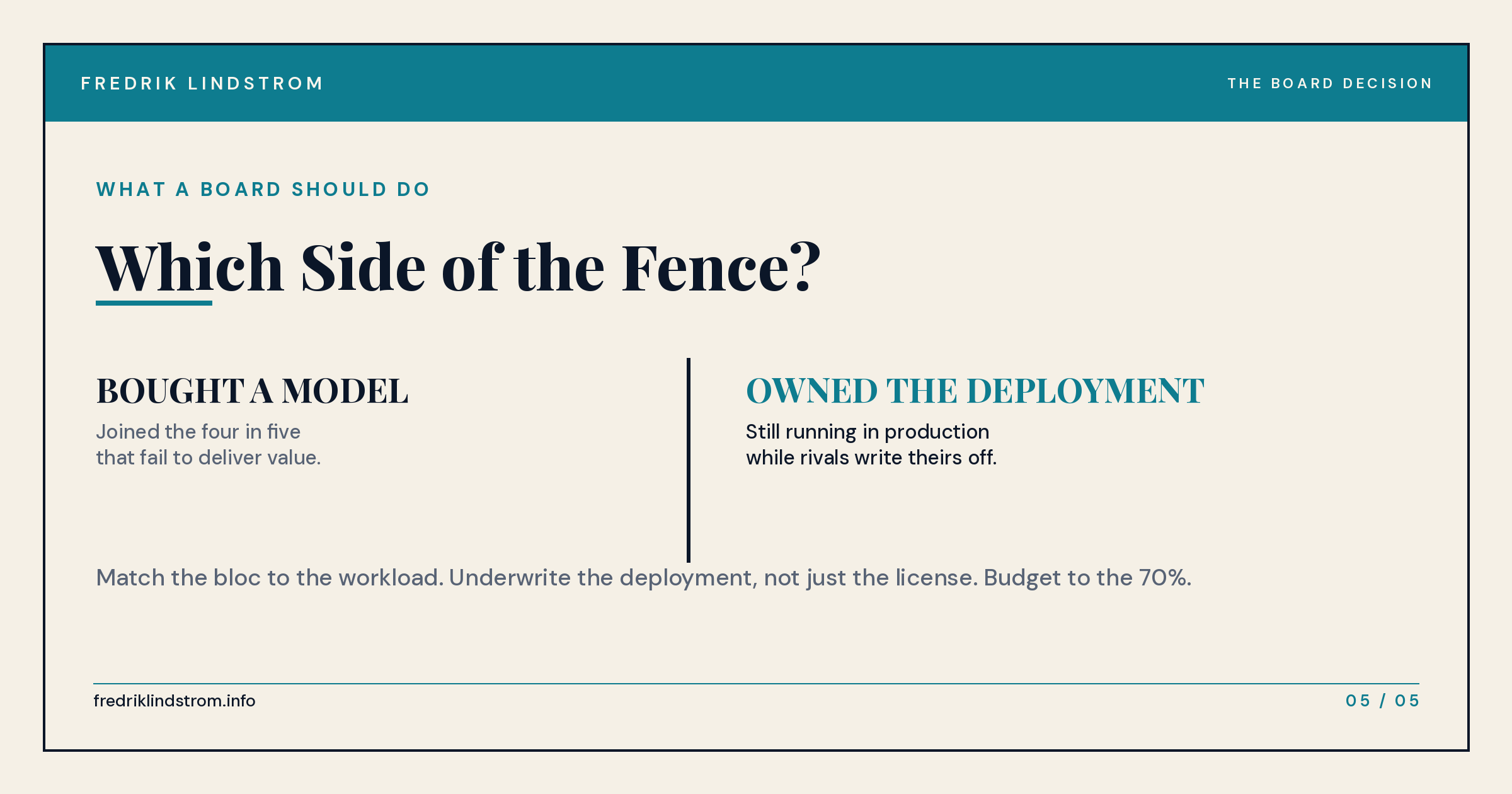

Underneath all three, budget to the 70%. If your AI program spends more than 60% on models and infrastructure and less than 40% on the people, process, and deployment work around them, you have built it to fail before you have chosen a vendor. Treat the vendor’s deployment and services capability as a first-order selection criterion, not an afterthought. Tie payment to production and to measured impact, not to a finished pilot, because the base rate says the pilot is where most of this dies.

And watch four thresholds over the next 18 months, because any of them resets the strategy. Whether the EU formally defers its high-risk deadlines. Whether the American IPO disclosures expose the revenue and margin questions as material. Whether China breaks its memory bottleneck and closes the compute gap faster than expected. And whether US federal law finally preempts the state patchwork and simplifies compliance.

The model layer is commoditizing in real time. The frontier will keep moving, the prices will keep falling, and within a year the gap between the blocs at the level most enterprises operate will be narrower than it is today. What will not commoditize is the 70% — the deployment, the governance, the discipline to take a capable model and make an organization able to stand behind what it does. That is the fence. On one side are the enterprises that bought a model and joined the four in five that fail. On the other are the ones that owned the deployment and are still running their AI in production while their competitors write theirs off.

Which side of the fence will your enterprise be on?

Sources

Figures and developments below were checked against the cited sources in June 2026. Where a claim rests on a single anonymous-sourced report (Mistral’s raise) or on vendor-published data (Chinese benchmarks), that is flagged in the text above.

The deployment gap

- RAND Corporation, The Root Causes of Failure for AI Projects (Ryseff, De Bruhl & Newberry, 2024) — the ~80% failure figure. https://www.rand.org/pubs/research_reports/RRA2680-1.html

- MIT Project NANDA, The GenAI Divide: State of AI in Business 2025 — 95% of GenAI pilots delivering no measurable return; external-partner builds outperforming internal ones. Report (PDF): https://mlq.ai/media/quarterly_decks/v0.1_State_of_AI_in_Business_2025_Report.pdf · Coverage: https://finance.yahoo.com/news/mit-report-95-generative-ai-105412686.html

- S&P Global Market Intelligence, Voice of the Enterprise (2025) — companies abandoning most AI initiatives rising from 17% to 42%. https://www.ciodive.com/news/AI-project-fail-data-SPGlobal/742590/

- Boston Consulting Group, Where’s the Value in AI? (2024) — the 10-20-70 principle. https://www.bcg.com/publications/2024/wheres-value-in-ai

United States

- Confidential IPO filings, June 2026 — Anthropic (June 1, ~$965B): https://www.foxbusiness.com/markets/anthropic-files-confidentially-ipo · OpenAI (June 8, ~$852B): https://techcrunch.com/2026/06/08/following-anthropic-openai-files-confidentially-for-ipo/

- The revenue/accounting dispute between the two labs: https://mezha.net/eng/bukvy/6fb39333_anthropic_files_confidential/

- The forward-deployed-engineering land grab — Anthropic’s $1.5B services JV (Blackstone, Hellman & Friedman, Goldman Sachs) and OpenAI’s “DeployCo”: https://techcrunch.com/2026/05/04/anthropic-and-openai-are-both-launching-joint-ventures-for-enterprise-ai-services/ · https://fortune.com/2026/05/04/anthropic-claude-consulting-industry-joint-venture-blackstone-goldman-sachs/

- Claude Fable 5 / Mythos 5 export-control suspension, June 2026 — Anthropic’s statement: https://www.anthropic.com/news/fable-mythos-access · Commerce Department directive (coverage): https://fortune.com/2026/06/13/anthropic-disables-fable-mythos-export-controls-national-security-threat/

Europe

- Mistral’s reported €3B raise at ~€20B valuation (Bloomberg, anonymous-sourced): https://techcrunch.com/2026/06/12/mistral-is-rumored-to-be-raising-e3b-at-e20-valuation/

- Owned-compute build-out — Sweden (€1.2B): https://www.bloomberg.com/news/articles/2026-02-11/mistral-invests-1-2-billion-in-swedish-ai-data-center-buildout · Paris data center ($830M debt; 200MW target by 2027): https://techcrunch.com/2026/03/30/mistral-ai-raises-830m-in-debt-to-set-up-a-data-center-near-paris/

- EU AI Act — Digital Omnibus provisional agreement (7 May 2026) deferring Annex III high-risk obligations to 2 December 2027 (EU Council press release): https://www.consilium.europa.eu/en/press/press-releases/2026/05/07/artificial-intelligence-council-and-parliament-agree-to-simplify-and-streamline-rules/ · Legal analysis: https://www.hoganlovells.com/en/publications/eu-legislators-agree-to-delay-for-highrisk-ai-rules

China

- Alibaba’s Qwen — 700M+ Hugging Face downloads, 113,000+ derivative models, over half of global open-source downloads: https://www.scmp.com/tech/big-tech/article/3349552/alibabas-qwen-family-captures-over-50-global-open-source-downloads-report-finds

- Chinese models passing US weekly token volume on OpenRouter (February 2026): https://eu.36kr.com/en/p/3700980530851712

- DeepSeek pricing and cost disruption: https://particula.tech/blog/deepseek-v4-qwen-open-source-ai-disruption

- Huawei Ascend and the high-bandwidth-memory bottleneck — RAND: https://www.rand.org/pubs/commentary/2025/08/leashing-chinese-ai-needs-smart-chip-controls.html · CSIS: https://www.csis.org/analysis/deepseek-huawei-export-controls-and-future-us-china-ai-race

- MiniMax and Zhipu Hong Kong IPOs (January 2026): https://restofworld.org/2026/zhipu-ai-minimax-ipo/